Chaotic Systems

or, why the market is a lot like the weather…

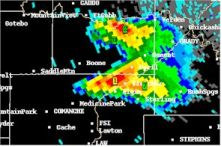

OK, it’s probably only in my fevered imagination that the two pictures above seem to bear a more than passing resemblance to each other. The one on the left is SmartMoney.com’s “map of the market” while the one on the right is a radar map of the storm-front that swept through Oklahoma in 1999, spawning 7 tornadoes as it went and doing $1.2 billion in damage.

I found myself contemplating the connection between weather and markets while reading the latest issue of Discover Magazine last night (Forecast: Hazy (with a 50% chance of error) Why making a science out of predicting the weather has been a lot harder than anyone guessed it would be By John Marchese). The most obvious similarity is that both the weather and the markets are very hard to predict, and largely for the same reasons. In both cases we’re dealing with complex, chaotic systems that are incredibly sensitive to “initial conditions.” The weather we will have in any given day, for example, is the result of interactions among countless billions of molecules in the air, the land, and the sea. The net effect of those myriad interactions could only be known with certainty if we could model the movements of every single one of those molecules in real-time, a feat still well beyond even the most advanced supercomputers.

Edward Lorenz, one of the fathers of chaos theory, was using computer simulations to study weather patterns in the 1960s when he discovered that changing the initial conditions for a given simulation – restarting it in the “middle” of a prior run and calculating the results to three decimal places instead of six – resulted in a vastly different outcome. In other words, very small changes in the starting point (“initial conditions”) will cause a chaotic system to go in a radically different – and unpredictable – direction. These findings caused Lorenz to ask the now-famous question:

“Can a butterfly flapping its wings in the Amazon Basin cause hurricanes over Kansas?”

Like the weather, the financial market behavior we observe in any given day is the result of untold billions of interactions between buyers and sellers, all reacting to information of every sort, including company financials, industry and economic conditions, politics, world events, you name it. The net result of these interactions will depend on the “initial conditions” in effect at any given moment, which is why you will so often see market commentators offer the same explanation for radically different market outcomes. For example, the Federal Reserve lowered the Fed Funds rate yesterday by a half a percentage point and the stock market went down. A few weeks ago, the Fed lowered interest rates and the market went up. Aren’t lower rates supposed to cause markets to rise? Well, yes, all other things being equal, as the economists like to say (actually, economists prefer the more imposing Latin phrase ceteris paribus). The simple fact is that all other things are never equal. So, unless you know the mind of every one of those 80 million or so traders, and can tally their thoughts in real-time, predicting short-term market movements is like predicting the weather three days out, an endeavor so problematic that the U.S. Weather Bureau, according to the Discover article, doesn’t even bother to keep statistics.

Does this mean that no useful statement can ever be made about the future course of the markets? Not at all! Chaotic systems, including the weather and the financial markets, are still open to “probabilistic” statements. That is, there are certain regularities that can be identified. For example, while it’s hard to say how much rainfall we’re going to have in a given year, you might start by looking at the average for the last ten or twenty years. While this year’s rainfall will almost surely be higher or lower than the long-run average, with each passing year the cumulative precipitation will begin to approach that “normal” value (a phenomenon known as “reversion to the mean”). Likewise, many academics believe that the stock markets can be characterized as following a “mean reverting” process. This means that investors with longer time horizons – five to ten years or more – don’t need to predict the market’s movements from one year to the next; they can make plans based on the average expected results over their full investment period. While it’s true that you’ll still be subject to “initial conditions” – that is, you’ll have a better outcome ten years down the line if you started with a winning year than if you’d gotten off to a “losing start” – you’re still likely to experience certain regularities. Such as the fairly-certain expectation that over ten years or longer your stock investments will yield a return higher than those available from “safe” investments like CDs and money market funds. Another way of putting this is to say that, while the return to the stock market over any given ten year period will be different, it will almost always be higher than the alternatives.

What more do you need to know?